Banking revenue growth has been particularly strong in the regions around the Indian Ocean, including India. This “Indo-Crescent” region now hosts 51% of the world’s top-performing financial institutions. The Indian banking sector, alongside other regional markets, benefits from higher GDP and population growth, as well as innovative disruptions and efficient service delivery models. The report underscores the strategic necessity for banks to leverage advanced technologies, such as artificial intelligence (AI), adapt to evolving risks, and navigate the recent rise in interest rates.

These factors have enhanced net interest margins and profitability, though challenges persist with capital-light business models and regulatory pressures. By integrating these global insights with a detailed analysis of the Indian banking sector and UBI’s performance, this chapter offers a holistic view of the banking industry’s current state and future trajectory. This enriched perspective is designed to help stakeholders understand both local and international factors influencing the sector, thereby enabling more informed strategic decisions.

Banking Industry Structure

Classification of Banks in India

Scheduled Banks: India’s banks encompass commercial and cooperative banks. These banks are included in the Second Schedule of the Reserve Bank of India Act, 1934, and meet certain criteria stipulated by the Reserve Bank of India (RBI).

- Commercial Banks: Commercial banks in India are categorized into public

sector banks, private sector banks, foreign banks, and small finance banks.

These banks engage in various banking activities, including accepting deposits,

providing loans, and offering financial services to individuals, businesses, and

governments.

- Public Sector Banks (PSBs): Public sector banks, including major entities like the Union Bank of India, play a crucial role in the Indian banking landscape, particularly in rural and semi-urban areas. These banks are majority-owned by the government and contribute significantly to financial inclusion and economic development.

- Private Sector Banks: Private sector banks compete with public and foreign banks, offering various financial products and services. These banks are primarily owned by private entities, focusing on efficiency and innovation to attract customers.

- Foreign Banks: Foreign banks operate in India through branches or wholly-owned subsidiaries, contributing to the diversity of the banking sector. They bring global best practices and advanced banking technologies to the Indian market.

- Small Finance Banks: Small finance banks are established to serve underserved sections of society, promoting financial inclusion by providing savings vehicles and supplying credit to small business units, small and marginal farmers, micro and small industries, and other unorganized sector entities.

- Cooperative Banks: Cooperative banks are divided into urban and rural cooperative banks. These banks function on cooperative principles, providing banking services primarily to economically weaker sections of society.

- Urban Cooperatives: Urban cooperative banks operate in urban and semi-urban areas, offering credit facilities to small businesses, traders, and individuals. They play a vital role in catering to the banking needs of local communities.

- Rural Cooperatives: Rural cooperative banks are instrumental in serving the agricultural sector and rural communities. They provide essential banking services and credit support to farmers, agricultural labourers, and rural artisans, promoting rural development and agricultural productivity.

Union Bank of India: An Overview

Union Bank of India (UBI) was nationalized in 1969, significantly expanding its reach into rural and semiurban areas. This pivotal moment in the bank’s history enabled it to extend services to a broader population and support various government initiatives aimed at financial inclusion and rural development. A significant milestone in UBI’s history was the merger in 2020, where Andhra Bank and Corporation Bank were amalgamated into Union Bank of India. This merger has enhanced UBI’s operational capabilities, customer reach, and financial strength, positioning it as one of the largest banking networks in the country.

Union Bank of India has a substantial presence in rural and semi-urban areas, playing a crucial role in supporting financial inclusion. The Bank’s extensive network ensures that banking services are accessible to underserved communities, facilitating economic development and poverty alleviation in these regions.

UBI offers a comprehensive suite of banking products and services designed to meet the diverse needs of its customers. These include savings accounts, various types of loans, insurance products, and investment services. The Bank continuously innovates to provide tailored solutions, ensuring that it meets the evolving demands of its customer base.

UBI’s Role in the Indian Banking Structure

Union Bank of India (UBI) plays a pivotal role within the Indian banking structure, particularly as a major entity among Public Sector Banks (PSBs). As a PSB, UBI is majority-owned by the Government of India. It plays a critical role in implementing government policies and financial inclusion initiatives. The Bank operates extensively in rural and semi-urban areas, providing essential banking services to a broad population segment, including underserved communities.

UBI’s strong presence in rural and semi-urban areas helps bridge the gap between urban and rural banking services. The Bank supports agricultural financing, small and medium enterprises (SMEs), and various government schemes to boost economic development at the grassroots level.

UBI is instrumental in driving financial inclusion in India. It participates in numerous government programs, such as Pradhan Mantri Jan Dhan Yojana (PMJDY), which aims to give every household access to banking services and a basic savings account. UBI also offers financial literacy programs to educate the rural population about banking services and digital banking.

As a PSB, UBI offers various financial products and services, including personal banking, corporate banking, international banking, and treasury operations. This diversification helps meet the varied needs of its customer base, ranging from individuals to large corporations.

Strategic Initiatives and Technology Adoption

UBI has embraced digital transformation to enhance its service delivery and operational efficiency. The Bank has invested in technology to provide internet banking, mobile banking, and other digital services, making banking more accessible to its customers. UBI has formed strategic alliances and partnerships to expand its reach and improve its service offerings. These alliances help UBI leverage new technologies and innovative solutions to stay competitive in the evolving banking landscape.

Contribution to Economic Development

Union Bank of India (UBI) is deeply committed to contributing to India’s economic development by supporting small and medium enterprises (SMEs), which are crucial for the country’s growth. The Bank offers specialized financial products, including working capital loans, term loans, and tailored solutions that cater to the unique needs of SMEs, fostering entrepreneurship and innovation.

In the agricultural sector, UBI plays a vital role by providing loans and credit facilities to farmers. These financial services help farmers purchase equipment, seeds, and fertilizers, and manage their seasonal cash flow needs. The Bank also supports agro-based industries and promotes sustainable agricultural practices through financial inclusion and education.

UBI offers a comprehensive range of personal finance products to cater to individual financial needs. These include savings accounts, as well as personal, home, and educational loans. By providing accessible and affordable financial solutions, UBI helps individuals achieve their personal and professional goals, contributing to the overall economic well-being of the communities it serves.

UBI is also committed to sustainable banking practices and corporate social responsibility (CSR). The Bank finances renewable energy projects and supports green initiatives, promoting environmental sustainability. Additionally, UBI’s CSR activities include supporting education, healthcare, and community development projects, reflecting its role as a responsible corporate citizen dedicated to improving the quality of life for the underprivileged.

Through its commitment to green finance, UBI actively funds renewable energy projects and sustainable practices, helping to reduce environmental impact and supporting India’s transition to a sustainable economy. Union Bank of India plays a crucial role in India’s economic development by supporting SMEs, agriculture, and personal finance. Its dedication to sustainability and green finance ensures that growth benefits all segments of society.

Global Banking Dynamics

The global banking industry has experienced significant changes in the financial year 2023-24, marked by remarkable performance and substantial challenges. According to McKinsey’s Global Banking Annual Review 2023, the past 18 months have been among the best for banks’ return on equity (ROE) in more than a decade. The ROE rose to 12% in 2022 and is expected to reach 13% in 2023, significantly higher than the 13-year average of 9.1%. This improvement was driven by a 500-basis-point increase in interest rates in developed economies since the second quarter of 2022, which boosted net interest margins and sector profits by approximately $280 billion.

Key Trends Shaping the Banking Landscape

Indian Banking Industry Dynamics

The financial year 2023-24 was marked by robust credit and deposit growth across major sectors in India. This period saw a significant improvement in asset quality, reflecting a strengthened banking sector better equipped to manage and mitigate lending risks. Increased credit availability supported various economic activities, fostering industrial growth and contributing to overall economic stability. Amidst global financial challenges, the Indian banking sector demonstrated resilience and effective transmission of monetary policy adjustments. These dynamics not only bolstered economic growth but also ensured the stability and confidence of the financial system in India.

Deposit Growth and Policy Rate Transmission

The policy repo rate was increased by 250 basis points from May 2022 to February 2023 tightening the monetary policy in order to curtail inflation. During FY 2023- 24, deposit growth clocked 12.9%, way above the nominal GDP growth of 9.6% on the back of efficient transmission of 250 basis point rate hike into deposit rates as banks faced the need to fund rising credit demand. The ability of banks to attract and retain deposits despite rising interest rates underscores the sector’s robustness and the effective management of interest rate risks.

Resilience Amidst Global Financial Changes

The Indian banking sector demonstrated remarkable resilience amidst global financial challenges throughout FY2024. Significant economic uncertainties and financial volatilities on the worldwide stage characterized this period. Indian banks managed to maintain adequate capital buffers, ensuring financial stability and instilling confidence among stakeholders. Furthermore, the sector maintained moderate non-performing loans (NPLs), indicating effective credit risk management practices and a sound regulatory environment.

Policy Repo Rate Adjustments

During FY 2023-24, the Monetary Policy Committee (MPC) kept the policy repo rate unchanged at 6.50% and remained resolute in its commitment to align inflation with the target, keeping in mind the objective of growth. The 250 basis points hike made during FY2022-23 contributed to control inflationary pressures and stabilize the economy amidst global and domestic challenges. The same is reflected in headline CPI inflation moderating from an average of 6.7% in 2022-23 to 5.4% in 2023-24 in response to monetary policy actions.

Impact on Money Market and Repo Rate Transmissions

The adjustments in the policy repo rate had a noticeable impact on money market rates, indicating effective monetary policy transmission. Money market rates aligned closely with the changes in the repo rate, demonstrating the RBI’s influence on the broader financial system. This alignment facilitated effective transmission to bank lending and deposit rates, ensuring that the policy measures had the intended effect on the economy. The responsiveness of money market rates to repo rate changes highlights the efficiency of the monetary policy framework in India.

FY2024 Performance of Union Bank of India

Union Bank of India (UBI) experienced stable credit and deposit growth throughout the fiscal year 2023-24, underscoring its strong market position and effective management. This period also marked significant improvements in asset quality and profitability metrics, indicating the bank’s enhanced ability to manage risk and generate returns.

Credit and Deposit Growth

UBI experienced stable credit and deposit growth, with gross advances increasing by 11.73% YoY to ₹ 9,04,884 crore and total deposits growing by 9.29% YoY to ₹ 12,21,528 crore as of March 31, 2024. This growth was driven by significant expansions in the retail, agricultural, and MSME (RAM) segments, which collectively saw a 13.82% increase YoY.

Asset Quality and Profitability

Improvements in asset quality and profitability were significant. The Bank’s Gross NPA ratio reduced by 277 basis points YoY to 4.76%, while the Net NPA ratio decreased by 67 basis points to 1.03% as of March 31, 2024. This reflects UBI’s enhanced ability to manage credit risks effectively. Net profit for FY2024 stood at ₹ 13,648 crore, a substantial increase from ₹ 8,433 crore in the previous fiscal year, indicating a 61.84% YoY growth.

For a more comprehensive analysis of these performance metrics, refer to the chapters on Manufactured and Financial Capitals in this report.

Challenges and Risks in the Banking Sector

UBI’s approach to addressing challenges and risks demonstrates its commitment to maintaining a resilient and secure banking environment. The Bank’s strategic initiatives in cybersecurity, operational risk management, regulatory compliance, asset quality improvement, and sustainability underscore its dedication to safeguarding stakeholder interests and supporting long-term economic stability.

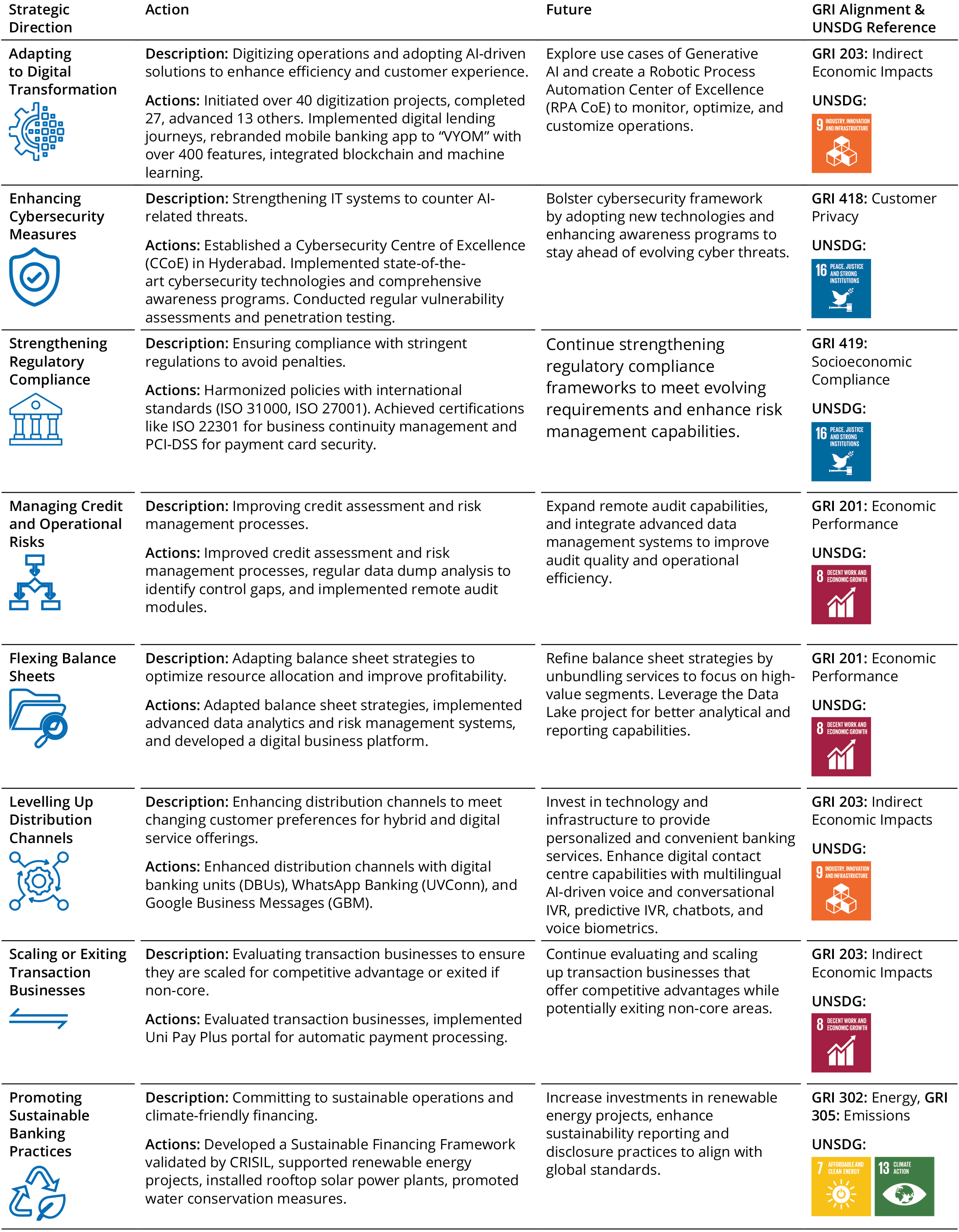

Digital Disruption and Cybersecurity Risks

The increasing reliance on digital transactions has heightened banks’ susceptibility to cyber threats. Union Bank of India (UBI) has acknowledged this risk and has taken proactive measures to safeguard its digital infrastructure. To mitigate these risks, UBI has established comprehensive cybersecurity measures. The Bank’s Cybersecurity Centre of Excellence (CCoE) in Hyderabad focuses on implementing cutting-edge cybersecurity technologies and running extensive awareness programs for employees and customers. This centre plays a crucial role in identifying and addressing potential cyber threats before they can cause significant damage.

Moreover, UBI conducts regular vulnerability assessments and penetration testing to identify and rectify weaknesses in its systems. These assessments help ensure that the bank’s defences are up-to-date and can thwart sophisticated cyber-attacks. By continually updating its cybersecurity protocols and investing in advanced security technologies, UBI demonstrates its commitment to maintaining the integrity and security of its digital infrastructure.

Operational Risks

Implementing advanced technologies, while essential for staying competitive, has introduced new operational risks. These risks include potential system failures, data breaches, and other bank operations disruptions. UBI has addressed these concerns by harmonizing its policies with international standards such as ISO 31000 for risk management and ISO 27001 for information security management. Additionally, the Bankconducts regular vulnerability assessments and penetration testing to identify and mitigate potential threats.

Implementing advanced technologies, while essential for staying competitive, has introduced new operational risks at Union Bank of India (UBI). These risks encompass potential system failures, data breaches, and other disruptions that could impact the bank’s operations. These efforts are part of a broader strategy to enhance operational resilience and safeguard the bank’s operations against evolving cyber threats. By adopting the best risk management and cybersecurity practices, UBI aims to protect its customers and maintain trust in its services.

Regulatory Compliance Challenges

Stricter regulations necessitate robust compliance frameworks within the banking sector. UBI has responded by ensuring compliance with various regulatory frameworks, including the RBI Cyber Security Framework, Digital Payment Security Controls, and IT Governance and Risk Management guidelines. The Bank has also achieved certifications such as ISO 22301 for business continuity management and PCI-DSS for payment card security, which help maintain high regulatory compliance standards.

Asset Quality and Credit Risks

Persistent issues with non-performing assets (NPAs) due to high corporate and agricultural debt levels remain a significant challenge for UBI. The Bank has focused on improving asset quality by adopting robust credit risk assessment mechanisms and adhering to responsible lending practices. In FY2024, UBI implemented a system for regular data dump analysis to identify and address control gaps, thereby enhancing the accuracy and completeness of its data. In FY2024, UBI made substantial progress in asset quality improvement. The Gross NPA ratio decreased to 4.76%, and the Net NPA ratio reduced to 1.03%. The Provision Coverage Ratio (PCR) improved to 92.69%, reflecting the bank’s commitment to maintaining a strong financial position and mitigating credit risks.

Sustainability Concerns

Banks are increasingly pressured to align their loan portfolios with climate-friendly projects. UBI has recognized the importance of sustainability and has taken steps to support environmental conservation initiatives. The Bank has adopted green technologies and eco-friendly infrastructure, promoting energy efficiency and reducing its carbon footprint. These efforts help mitigate environmental risks and enhance the bank’s reputation as a responsible corporate citizen.

Union Bank of India has recognized the importance of sustainability and has actively taken steps to support environmental conservation initiatives. The Bank has established an independent ESG Cell to drive its ESG journey, ensuring effective implementation of sustainability initiatives. UBI has developed a sustainable financing framework validated by CRISIL that covers products such as green deposits, green bonds, and sustainability-linked loans. Additionally, UBI has adopted green technologies and eco-friendly infrastructure, promoting energy efficiency and reducing its carbon footprint. These efforts not only help mitigate environmental risks but also enhance the bank’s reputation as a responsible corporate citizen.

Directions for Union Bank of India

In an era of rapid technological advancements and shifting market dynamics, the Union Bank of India (UBI) has continually adapted its strategies to maintain competitiveness and enhance service delivery. Recognizing the critical need to respond proactively to these changes, UBI has implemented a series of strategic initiatives to leverage technology, strengthen cybersecurity, ensure regulatory compliance, manage risks, and promote sustainability. These efforts are pivotal for the bank’s growth and efficiency and crucial in meeting the evolving needs of its customers and stakeholders.

Union Bank of India’s strategic emphasis on digital transformation and integrating AI and machine learning into operations highlights its commitment to streamlining processes, enhancing customer engagement, and reducing operational costs. The Bank’s proactive approach to cybersecurity, stringent regulatory compliance, and advanced risk management systems ensure robust protection and operational integrity. By optimizing balance sheet management, evaluating transaction businesses, and enhancing distribution channels, UBI aims to meet changing customer preferences and improve profitability. Furthermore, its investment in sustainable banking practices and renewable energy projects underscores its commitment to environmental sustainability and corporate responsibility. These strategic directions demonstrate UBI’s comprehensive approach to navigating modern banking complexities, driving growth, ensuring compliance, and fostering sustainability.